Abstract

In this paper, we map the growth cycle synchronization across the European Union, specifically focusing on the position of the Visegrad Four countries. We study the synchronization using frequency and time–frequency domain. To accommodate for dynamic relationships among the countries, we propose a wavelet cohesion measure with time-varying weights. Analyzing quarterly data from 1995 to 2017, we show an increasing co-movement of the Visegrad Four countries with the European Union after the countries have accessed the European Union. We show that participation in a currency union increases the co-movement of the country adopting the Euro. Furthermore, we find a high degree of synchronization at business cycle frequencies of the Visegrad Four and countries of the European monetary union.

Similar content being viewed by others

Notes

The Eastern Bloc was generally formed of the countries of the Warsaw Pact (as Central and Eastern European countries) and the Soviet Union.

The Visegrad Four countries also joined the North Atlantic Treaty Organization in 1999 and applied for membership in the European Union in 1995–1996.

These group consists of Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal, and Spain. We analyze this group and the V4 countries.

Characteristics of locally stationary time series are close to the stationary ones at each point of time or shorter periods.

This also overcomes the problem of short-time Fourier transform, or windowed Fourier transform (Gabor 1946).

It is possible to use methods of evolutionary spectra of non-stationary time series developed by Priestley (1965). However, to study time-varying dynamics we need to give up some frequency resolution, which is not the case when using wavelet techniques.

In “Appendix” in ESM, we demonstrate the wavelet-based measure (Eq. 3) in two particular cases, as shown in Fig. A.2.

Another possibility for testing the significance is area-wise test approach of Maraun et al. (2007).

To obtain the confidence intervals of frequency cohesion, we follow the procedures of Franke and Hardle (1992) and Berkowitz and Diebold (1998), where instead of bootstrapping the cohesion measure we bootstrap each (cross-)spectrum. Schüler et al. (2017) used this approach in their power cohesion measure while studying financial cycles for G-7 countries.

Data were obtained via OECD Database, May, 2018.

The V4 countries are included in the EU-28; however, the contribution is minimal to change the EU GDP growth. For robustness check, we analyzed the co-movement of the V4 and the EA-19 GDPs, and these results are almost identical to those we report.

Short periods of co-movement appear around and prior to 2000 at 1–2-year, and 2-year cycles, respectively, between Hungary and Slovakia, and Poland with the Czech Republic and Slovakia.

We have additionally checked the co-movement of the V4 countries and the Euro area of 19 countries (EA-19) as a proxy of the EU. The results are almost indistinguishable.

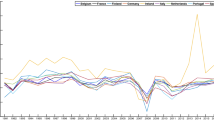

Poland’s economy share of agriculture in GDP is one of the higher.

Two countries are in-phase if the phase difference belongs to \([-\pi /2, \pi /2]\); otherwise, they are in the anti-phase. Moreover, the first country leads the second, \(x_j\), if the phase is in \([0, \pi /2]\) and \([-\pi , -\pi /2]\); when in \([-\pi /2, 0]\) and \([\pi /2, \pi ]\), the second country is leading.

Furthermore, the phase is more volatile when the coherence is low.

We should also carefully interpret the phase difference at 3–8-year cycles because of the cone of influence, which affects influences results at 8 years from both sides of the sample.

The figures of wavelet cohesion, heatmaps, display the results the same way as those of the wavelet coherence, except that the scale of the cohesion may be negative. Hence, the blue color depicts the negative relationship between economies, which may also be strong.

In “Appendix Fig. A.1” in ESM, we provide complementary results showing cohesion of the EU-12 countries (a) and peripheral countries (b), where both show much lower synchronization than the EU core in Fig. 6.

References

Aguiar-Conraria L, Soares MJ (2011a) Business cycle synchronization and the Euro: a wavelet analysis. J Macroecon 33(3):477–489

Aguiar-Conraria L, Soares MJ (2011b) The continuous wavelet transform: a primer. Technical report NIPE-Universidade do Minho

Aguiar-Conraria L, Soares MJ (2014) The continuous wavelet transform: moving beyond uni- and bivariate analysis. J Econ Surv 28(2):344–375

Aguiar-Conraria L, Azevedo N, Soares MJ (2008) Using wavelets to decompose the time–frequency effects of monetary policy. Phys A Stat Mech Appl 387(12):2863–2878

Aguiar-Conraria L, Martins MM, Soares MJ (2018) Estimating the taylor rule in the time–frequency domain. J Macroecon 57:122–137

Antal J, Hlaváček M, Holub T (2008) Inflation target fulfillment in the Czech Republic in 1998–2007: some stylized facts. Czech J Econ Finance (Finance a uver) 58(09–10):406–424

Artis MJ, Marcellino M, Proietti T (2004) Characterizing the business cycle for accession countries. In: CEPR discussion papers 4457

Backus DK, Kehoe PJ, Kydland FE (1992) International real business cycles. J Polit Econ 100(4):745–775

Baxter M, King RG (1999) Measuring business cycles: approximate band-pass filters for economic time series. Rev Econ Stat 81(4):575–593

Bekiros S, Nguyen DK, Uddin GS, Sjö B (2015) Business cycle (de) synchronization in the aftermath of the global financial crisis: implications for the Euro area. Stud Nonlinear Dyn Econom 19(5):609–624

Berkowitz J, Diebold FX (1998) Bootstrapping multivariate spectra. Rev Econ Stat 80(4):664–666

Bruzda J (2011) Business cycle synchronization according to wavelets-the case of Poland and the Euro zone member countries. Bank i Kredyt 3:5–31

Cazelles B, Chavez M, Berteaux D, Ménard F, Vik JO, Jenouvrier S, Stenseth NC (2008) Wavelet analysis of ecological time series. Oecologia 156(2):287–304

Christiano LJ, Fitzgerald TJ (2003) The band pass filter. Int Econ Rev 44(2):435–465

Crespo-Cuaresma J, Fernández-Amador O (2013) Business cycle convergence in EMU: a first look at the second moment. J Macroecon 37:265–284

Croux C, Forni M, Reichlin L (2001) A measure of comovement for economic variables: theory and empirics. Rev Econ Stat 83(2):232–241

Crowley PM (2007) A guide to wavelets for economists. J Econ Surv 21(2):207–267

Crowley PM, Hallett AH (2015) Great moderation or “Will o’ the Wisp”? A time–frequency decomposition of GDP for the US and UK. J Macroecon 44:82–97

Crowley PM, Maraun D, Mayes D (2006) How hard is the euro area core?: an evaluation of growth cycles using wavelet analysis. Bank of Finland Research Discussion Paper No. 18/2006. https://ssrn.com/abstract=3164195

Darvas Z, Szapáry G (2008) Business cycle synchronization in the enlarged EU. Open Econ Rev 19(1):1–19

Daubechies I (1992) Ten lectures on wavelets, vol 61. SIAM, Philadelphia

De Haan J, Inklaar R, Jong-A-Pin R (2008) Will business cycles in the euro area converge? A critical survey of empirical research. J Econ Surv 22(2):234–273

Ferreira-Lopes A, Pina ÁM (2011) Business cycles, core, and periphery in monetary unions: comparing Europe and North America. Open Econ Rev 22(4):565–592

Fidrmuc J, Korhonen I (2006) Meta-analysis of the business cycle correlation between the Euro area and the CEECs. J Comp Econ 34(3):518–537

Franke J, Hardle W (1992) On bootstrapping kernel spectral estimates. Ann Stat 20(1):121–145

Frankel JA, Rose AK (1998) The endogeneity of the optimum currency area criteria. Econ J 108(449):1009–25

Gabor D (1946) Theory of communication. Part 1: the analysis of information. J Inst Electr Eng Part III Radio Commun Eng 93(26):429–441

Ge Z (2008) Significance tests for the wavelet cross spectrum and wavelet linear coherence. Ann Geophys 26(12):3819–3829

Grigoraş V, Stanciu IE (2016) New evidence on the (de) synchronisation of business cycles: reshaping the European business cycle. Int Econ 147:27–52

Grinsted A, Moore JC, Jevrejeva S (2004) Application of the cross wavelet transform and wavelet coherence to geophysical time series. Nonlinear Process Geophys 11(5/6):561–566

Harding D, Pagan A (2002) Dissecting the cycle: a methodological investigation. J Monet Econ 49(2):365–381

Hodrick RJ, Prescott EC (1981) Post-war U.S. business cycles: an empirical investigation. In: Discussion papers 451. Northwestern University, Center for Mathematical Studies in Economics and Management Science

Jagrič T (2002) Measuring business cycles-a dynamic perspective. Banka Slovenije, Prikazi in analize X/1, Ljubljana

Jiménez-Rodríguez R, Morales-Zumaquero A, Égert B (2013) Business cycle synchronization between Euro area and Central and Eastern European countries. Rev Dev Econ 17(2):379–395

Kolasa M (2013) Business cycles in EU new member states: How and why are they different? J Macroecon 38(Part B):487–496

Kutan AM, Yigit TM (2004) Nominal and real stochastic convergence of transition economies. J Comp Econ 32(1):23–36

Maraun D, Kurths J, Holschneider M (2007) Nonstationary gaussian processes in wavelet domain: synthesis, estimation, and significance testing. Phys Rev E 75(1):016707

Mundell RA (1961) A theory of optimum currency areas. Am Econ Rev 51(4):657–665

Nason GP, Von Sachs R, Kroisandt G (2000) Wavelet processes and adaptive estimation of the evolutionary wavelet spectrum. J R Stat Soc Ser B (Stat Methodol) 62(2):271–292

OECD (2018) Quarterly GDP (indicator). https://doi.org/10.1787/b86d1fc8-en. Accessed 2 May 2018

Priestley MB (1965) Evolutionary spectra and non-stationary processes. J R Stat Soc Ser B (Methodol) 27(2):204–237

Raihan SM, Wen Y, Zeng B (2005) Wavelet: a new tool for business cycle analysis. In: Federal Reserve Bank of St Louis working paper series (2005-050)

Rua A (2010) Measuring comovement in the time–frequency space. J Macroecon 32(2):685–691

Rua A, Silva Lopes A (2012) Cohesion within the Euro area and the US: a wavelet-based view. In: Banco de Portugal, working paper (4)

Schüler YS, Hiebert P, Peltonen TA (2017) Coherent financial cycles for g-7 countries: why extending credit can be an asset. In: ESRB working papers series

Torrence C, Compo GP (1998) A practical guide to wavelet analysis. Bull Am Meteorol Soc 79(1):61–78

Vacha L, Barunik J (2012) Co-movement of energy commodities revisited: evidence from wavelet coherence analysis. Energy Econ 34(1):241–247

Yogo M (2008) Measuring business cycles: a wavelet analysis of economic time series. Econ Lett 100(2):208–212

Acknowledgements

We are very thankful to the editor and referees for useful comments and suggestions. We would like to thank participants of two conferences for constructive discussions—the 2nd International Workshop on “Financial Markets and Nonlinear Dynamics” in Paris and Slovak Economic Association meeting in Košice.

Author information

Authors and Affiliations

Corresponding author

Additional information

We gratefully acknowledge the financial support from the Czech Science Foundation under the GA16-14151S Project as well as the support from the Grant Agency of Charles University (GAUK), under Project No. 366015.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Hanus, L., Vácha, L. Growth cycle synchronization of the Visegrad Four and the European Union. Empir Econ 58, 1779–1795 (2020). https://doi.org/10.1007/s00181-018-1601-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-018-1601-x