Abstract

Biological invasions are one of the top drivers of the ongoing biodiversity crisis. An underestimated consequence of invasions is the enormity of their economic impacts. Knowledge gaps regarding economic costs produced by invasive alien species (IAS) are pervasive, particularly for emerging economies such as India—the fastest growing economy worldwide. To investigate, highlight and bridge this gap, we synthesised data on the economic costs of IAS in India. Specifically, we examine how IAS costs are distributed spatially, environmentally, sectorally, taxonomically, temporally, and across introduction pathways; and discuss how Indian IAS costs vary with socioeconomic indicators. We found that IAS have cost the Indian economy between at least US$ 127.3 billion to 182.6 billion (Indian Rupees ₹ 8.3 trillion to 11.9 trillion) over 1960–2020, and these costs have increased with time. Despite these massive recorded costs, most were not assigned to specific regions, environments, sectors, cost types and causal IAS, and these knowledge gaps are more pronounced in India than in the rest of the world. When costs were specifically assigned, maximum costs were incurred in West, South and North India, by invasive alien insects in semi-aquatic ecosystems; they were incurred mainly by the public and social welfare sector, and were associated with damages and losses rather than management expenses. Our findings indicate that the reported economic costs grossly underestimate the actual costs, especially considering the expected costs given India’s population size, gross domestic product and high numbers of IAS without reported costs. This cost analysis improves our knowledge of the negative economic impacts of biological invasions in India and the burden they can represent for its development. We hope this study motivates policymakers to address socio-ecological issues in India and launch a national biological invasion research programme, especially since economic growth will be accompanied by greater impacts of global change.

Similar content being viewed by others

Introduction

Globally, biological invasion rates show no signs of saturation (Seebens et al. 2017), and continued increases are expected in the next three decades (Seebens et al. 2021). Biological invasions have eroded biogeographic realms (Capinha et al. 2015) and present a growing threat to ecosystems, potentially compromising their function, structure, and service provision (Pyšek et al. 2020). Invasive alien species (IAS) have also been identified as major drivers of species extinction (Bellard et al. 2016), and they disrupt phylogenetic and functional diversities (Suarez and Tsutsui 2008; Ricciardi et al. 2013) as well as cause regime shifts in recipient environments (Brooks et al. 2004). Consequently, human-mediated introduction, establishment and spread of IAS have been considered defining elements of the Anthropocene (Pyšek et al. 2020; Ricciardi et al. 2021). Notwithstanding biases at temporal, geographic and biological scales (Crystal-Ornelas and Lockwood 2020a), knowledge of the ecological impacts of IAS has accrued rapidly in recent decades (Kumschick et al. 2015; Crystal-Ornelas and Lockwood 2020b). Contrastingly, knowledge of socioeconomic effects has remained sparse, unstandardised and disparate across most scales until recently (Diagne et al. 2020a).

Where reported, economic impacts associated with IAS are burgeoning (e.g., Pimentel et al. 2001; Oreska and Aldridge 2011; Hoffman and Boradhurst 2016; Bradshaw et al. 2016). Although these earlier studies provided awareness and powerful incentives to increase expenditure on the management of IAS, they all focused on particular regions, habitat types and taxonomic groups. Overall, most countries have no comprehensive appraisals of the economic costs of IAS, precluding efficient allocation of resources to mitigate ecological and economic impacts (Lodge et al. 2016). Recently, however, the InvaCost database (Diagne et al. 2020b) was launched to tackle this critical knowledge gap and provide comparable means to assess the costs of IAS. The database has involved systematic retrieving, collating and standardising of reported economic costs of IAS, and has provided the first global assessment of the economic impacts of biological invasions (Diagne et al. 2021a). With costs recorded against numerous environmental, typological, temporal and spatial descriptors, this database provides a critical step towards comprehensive assessments (e.g., Africa, Diagne et al. 2021b; Asia, Liu et al. 2021; Europe, Haubrock et al. 2021a; North America, Crystal-Ornelas et al. 2021; South America, Heringer et al.2021).

India, a rapidly emerging developing economy, categorised as mega-biodiverse and home to four of the global biodiversity hotspots (Myers et al. 2000), has not yet benefited from such a national synthesis. Although several thousands of nonindigenous introduced species are reported from India (Sankaran et al. 2021), the most conservative estimates report 173 invasive plants (Reddy 2008; Botanical Survey of India) and 157 invasive animals (Government of India 2018). Pimentel et al. (2001) reported that the Indian economy suffers US$ 116 billion per year as a result of IAS. However, almost all costs reported in this study were potential costs rather than observed costs, and hence, questionable and critiqued (e.g., Hoagland and Jin 2006; Holmes et al. 2009). For example, agricultural loss costs incurred by invasive insects were estimated by considering the percentage of alien insect species in India, the percentage of crop productivity loss due to insects, the total crop production and its value in India. Based on these values, they attributed a yearly monetary loss of US$ 16.8 billion to agriculture by invasive insects. By missing robust, documented evidence for the economic impacts of IAS, gross overestimation of actual costs is likely to arise from studies relying on potential costs.

Despite the long-lasting ecological problems caused by IAS in India, the country lacks awareness of the enormity of associated economic costs, in turn preventing the development of biosecurity protocols, pre- and post-invasion monitoring guidelines, effective eradication programmes and trained human resources to tackle this issue (Mungi et al. 2019; Goyal et al. 2020). The most common examples of IAS in India include the Santa-Maria feverfew or carrot grass Parthenium hysterophorus, gaining entry with imported wheat from the USA in the 1950s (Ahmad et al. 2019); the flagship mass social afforestation programmes undertaken by the government of India using the invasive river tamarind Leucaena leucocephala; or the invasion of the Mozambique tilapia Oreochromis mossambicus, a fast-growing fish introduced as a source of income for disadvantaged fishing communities, but which is now replacing the native fish communities in Indian water bodies (Ganie et al. 2013).

While economic development and environmental conservation are often seen as two opposing sides of the development spectrum, quantifying the costs borne by a country due to invasions could be an effective way to attract the attention of policymakers and motivate measures against IAS. Here, we provide an exploratory, yet state-of-the-art analysis of the economic costs of IAS in India. Specifically, we aim to: (i) describe how IAS costs are distributed spatially, environmentally, sectorally, taxonomically, according to cost types and across introduction pathways; (ii) assess how IAS costs have changed over time, in particular concerning the type of costs (i.e., management versus damage); (iii) determine how IAS costs of India and other countries vary according to population sizes, GDPs and economic development statuses; and (iv) highlight the knowledge gaps in IAS costs in India.

Materials and methods

Data collection and processing

Data collection

Information on the economic cost of IAS in India was extracted from the InvaCost version 3.0 database (https://doi.org/10.6084/m9.figshare.12668570.v3; 9,823 entries; Diagne et al. 2020b, Diagne et al. 2020c; Angulo et al. 2021). The data in InvaCost were collected via (i) literature searches using the Web of Science, Google Scholar and the Google search and (ii) targeted searches through contacting experts and stakeholders to request additional cost information. To obtain costs specific to India from this database, we filtered costs based on the “Official_country” column of the database (see Online Resource 1), thereby excluding costs from other countries or at greater spatial scales (e.g., subcontinental or continental). We also omitted those costs from the InvaCost database that were jointly attributed to India and other countries without specifics on country-wise costs. Thus, the costs in the dataset used for this manuscript were incurred only in India.

To make the India data more comprehensive, we conducted additional literature searches and expert consultations. For literature searches, we identified documents with costs by reviewing literature published until March 2021 using all of the following methods: (i) employing the search strings considered by Diagne et al. (2020b), such that each search string had the words ‘invas*’ and ‘econom*’ and terms such as ‘exotic’, ‘alien’, ‘IAS’, ‘cost’, as well as the most commonly-used currencies such as ‘USD’ or ‘$’, but also adding ‘India’, ‘Rupee’, ‘INR’ or ‘₹’; (ii) adding common and scientific names of the 21 high concern invasive species (HiCIS) from India (Mungi et al. 2019) to retrieve species-specific costs; (iii) streamlining the search process further by advanced Google search options and specifying the region as ‘India’ and the language as ‘English’ or ‘Hindi’, to retrieve English and non-English language results located on Indian websites and servers. Only those documents were included in the analysis that mentioned at least one cost record and where the cost records were explicitly attributed to IAS. Costs attributed jointly to IAS and other species were not considered in the analysis.

For expert consultations, we contacted 20 IAS experts by e-mail, both managers and researchers, throughout India such that each of the six administrative regions in India (Northern, Central, Southern, Eastern, Northeastern and Western India) was represented by at least one expert on invasive plants, invertebrates and vertebrates. It was done to achieve a balanced representation of regions and taxa within the country in our analysis, to ensure we did not miss any published source. We did not use a formal questionnaire, but kept the communication open-ended to encourage reporting of documented costs for a diverse range of taxa.

Database structure and data authentication

The database comprised of more than 50 cost-related variables (Online Resource 1, sheet “Variables_Info”), broadly classified into the following six categories: (i) the bibliographic information of the document where the costs were reported (e.g., author, year, type of article, language, among others), (ii) taxonomic information of the IAS causing cost, (iii) geographical and environmental information of the impacted area, (iv) temporal information on the year and the duration of the cost, (v) economic information on raw and standardised cost values, and (vi) the sectoral and typological information on the impact of the IAS. For additional details on these various categories and the overall database, see Diagne et al. (2020b).

For each entry, raw cost data in the local currency, as mentioned in the original retrieved document, were entered into the database (column “Raw_cost_estimate_local_currency”, see Online Resource 1). In case a single cost entry was represented by a range of values, the minimum and maximum costs were entered in the database (columns “Min_raw_cost_estimate_local_currency” and “Max_raw_cost_estimate_local_currency”, see Online Resource 1) and their mean was taken as the raw cost datum. Multiple unique costs from the same document were entered as multiple cost entries with their unique descriptors, one in each row, and not as a single pooled cost for the entire document. To avoid overestimation of costs, data were screened for possible errors, duplicates and overlaps. InvaCost records costs whilst explicitly considering their source material, reliability (i.e., classification of cost estimates based on the type of publication and method of estimation; Low vs. High) and implementation approach (i.e., Observed vs. Potential). The reliability of the source material was (i) High if either provided by officially pre-assessed materials (peer-reviewed articles and official reports) or the estimation method was documented, repeatable and/or traceable if provided by other grey literature, or (ii) Low if reported in unofficial and non-assessed documents or if the estimation method was not documented. Furthermore, the costs were considered as (i) Observed if actually incurred (money was spent or damages and losses were monetised), or (ii) Potential if not incurred but expected or predicted.

The variables on temporal information of the costs, i.e., the year in which the cost was incurred and the duration of the cost, were important for the further cost analysis and were retrieved from the original documents. These variables included (i) “Period_of_estimation” (referring to the year or the range of years in which the cost was incurred), (ii) “Time_range” (referring to the duration of the cost, as “Year” if the cost was yearly or less than a year, and “Period” for costs spanning multiple years), and (iii) “Probable_starting/ending_year” (referring to the exact year or period in which the cost was incurred). The raw cost estimates were converted to annual costs (column “Cost_estimate_per_year_local_currency”) by dividing the cost by the number of years for which the cost was incurred. Thus, for “Period” costs ranging multiple years, the raw cost was divided by the difference between the “Probable_ending_year” and “Probable_starting_year”. For “Year” costs, since the cost was incurred in a single year, the raw cost value was taken as the annual cost (for all these variables, see Online Resource 1).

Cost standardisation

All costs were converted and adjusted for inflation from local currencies to 2017 US Dollars (US$). This standardisation and conversion was done in two ways: one, based on the market exchange rate (local currency unit per US$, calculated as an annual average) for the specific year in which the cost was reported, and another, the purchasing power parity (PPP, local currency unit per US$, calculated as an annual average) i.e., the rate of currency conversion that standardises the purchasing power of different currencies by eliminating the differences in price levels between countries. All further cost analyses were performed using the costs expressed by exchange rate information (column “Raw_cost_estimate_2017_USD_exchange_rate”, see Online Resource 1).

Each cost was converted from the local currency to US$ by dividing the raw cost by the official market exchange rate (https://data.worldbank.org/indicator/PA.NUS.FCRF?end=2017&start=1960) corresponding to the year of the cost estimation (column “Applicable_year” in Online Resource 1, that is the year of the cost reporting, and not necessarily the year of cost occurrence). The cost obtained in US$ of that year was then converted to the 2017 value of US$ (for more details, see Diagne et al. 2020b).

Costs in InvaCost are reported over different durations (e.g., several months, single years or several years). Therefore, we standardised costs such that each cost entry corresponded to a single year. Cost standardisation was done using the expandYearlyCosts function of the ‘invacost’ R package (Leroy et al. 2021), thereby ‘expanding’ the data based on the difference between the “Probable_starting_year_adjusted” and “Probable_ending_year_adjusted” columns for each cost entry (see Online Resource 1). For example, a cost of US$ 1,000,000 over 5 years was transformed into five annual entries, each of US$ 200,000 over those 5 years. We removed cost entries that occurred outside of the 1960–2020 time range, given official data needed for standardising costs to a unique currency were not available before (Diagne et al. 2020b). We also removed cost entries for which the starting and/or the end year were not specified. This removal process resulted in the omission of some highly prominent entries, such as Pimentel et al. (2001). However, we deemed these omissions necessary to annualise costs according to that year’s currency exchange rate and to produce reliable projections of temporal trends.

Distribution of IAS costs

Using the descriptors present in the InvaCost database (see above), we deciphered the distribution of IAS costs following the (i) spatial scale (i.e., national or restricted to a specific region of the country); (ii) environment of the IAS (i.e., terrestrial, aquatic or semi-aquatic; column “Environment_IAS”, see Online Resource 1); (iii) sector impacted (i.e., agriculture, authorities-stakeholders, environment, fishery, forestry, health and public and social welfare; column “Impacted_sector”, see Online Resource 1); (iv) taxonomic group (i.e., Kingdom, Class, Order, Family, Genus or Species; columns “Kingdom/Class/Order/Family/Genus/Species”, see Online Resource 1); and (v) across introduction pathways.

Temporal trends

We evaluated the temporal trends of IAS costs (from 1960 to 2020) in relation to the type of costs (i.e., management vs damage; column “Type_of_cost_merged”, see Online Resource 1). Damage expenditures included impact-related costs, such as infrastructure losses, health issues and reduction in ecosystem productivity, whereas management-related costs included mitigation costs, such as prevention, control, eradication, research and long-term management of IAS. To conduct this analysis, we used the summarizeCosts function of the invacost package (Leroy et al. 2021) that produced the average annual cost at 10-year intervals and annual totals, and thus allows for the discernment of cost trajectories over time. Further, we used the modelCosts function of the same R package to statistically model the long-term trends in invasion costs, fitting ordinary least squares (linear/quadratic) and robust (linear/quadratic) regressions, which is less sensitive to outliers, as well as multivariate adaptive regression splines, generalised additive models and quantile regressions. Multiple models were fit to discern generalities in trends over time, given the heteroskedasticity of econometric data. Given delays in the occurrence of impact and the publication of this impact in monetary terms, we examined time lags between the “Impact_year” and “Publication_year” in our data, removing years with a cost completeness of 75% or less based on the quantiles of this relationship. As such, costs up until the year 2013 were included in the analysis, with the remaining years excluded from the models.

Cost extrapolation for IAS with no recorded costs in India

To assess potential costs of IAS that occur in India, but have no cost data record for India in InvaCost version 3.0 and the targeted searches, we performed a preliminary approximation of these costs as follows. We created a list of IAS from India by retrieving species designated as ‘invasive’ in the Global Register of Introduced and Invasive Species (GRIIS), the Global Invasive Species Database (GISD), and the 21 HiCIS for India (Mungi et al. 2019). Species that are considered ‘alien’ in India, but whose invasion status was categorised as ‘Uncertain’, ‘Unspecified’, ‘Null’, or ‘Cryptogenic’ by GRIIS and GISD, were not included in this analysis. This was done to remain conservative in our cost estimates by including only those species whose invasion status was confirmed in India.

This resulted in three separate lists of 282 IAS from GRIIS, 51 from GISD and 21 from the HiCIS. We then combined these three lists by removing the overlaps and synonyms, resulting in 330 IAS with confirmed invasion status in India. Subsequently, we searched for costs attributed to these species in the InvaCost version 3.0 database. Once again, we adopted a conservative approach, by focusing only on Observed and High reliability costs. We found 54 out of the confirmed 330 IAS in India that had cost entries from other countries in the world, but not from India.

Second, we compiled a list of species in our database (InvaCost version 3.0 plus targeted searches, Online Resource 1) that had attributable costs (Observed and High reliability costs only) simultaneously from India and from outside India. We found five such species that had incurred costs from both within and outside India. We logn transformed these five species’ costs, and established a linear regression model consisting of India costs as a function of the non-India global costs for each of these species. Finally, following the methodology applied in a previous work (Renault et al. 2021) we extrapolated this cost relationship, between the Indian and the non-Indian global costs of the same IAS, to calculate potential costs of IAS in India that have no recorded costs in India but have incurred costs outside India.

Association with socioeconomic status

To examine how economic costs of IAS in India relate to other countries with reported economic costs included in the InvaCost database (for details of countries considered here, see Diagne et al. 2020c; data extracted from ‘invacost’ R package, Leroy et al. 2021) highly reliable, observed costs of all other countries in the InvaCost database (n = 112) were totalled (1960–2020) and compared in relation to total human population and GDP using data from worldometers (https://www.worldometers.info/world-population/population-by-country/) for population and The World Bank (https://data.worldbank.org/indicator/NY.GDP.MKTP.CD) for GDP (2019 value). We note that cost reporting for certain countries started later (or earlier) than 1960, but from 1960 allowed for robust exchange rate calculations. The economic development status (developed, transitioning, developing) of each country was obtained and characterised from the United Nations (2020) categorisation. Two linear models were used to examine the relationship between logn transformed total costs and (i) logn transformed total population and (ii) logn transformed GDP, with development status included as an interaction term in each two-way model, allowing to compare the economic cost of IAS in India with those of other countries.

Identification of knowledge gaps

To investigate differences between the distribution of costs in India with the global trends, we compared the India dataset (Online Resource 1) with non-India cost entries in InvaCost 3.0. To build this dataset containing non-India data, we first excluded all India-based costs from InvaCost 3.0, including costs that were reported at the subcontinental scale, entered as “Bangladesh/India/Pakistan” or “India/Pakistan” in the “Official_country” column. This resulted in an exclusive non-India dataset. Next, we excluded Potential and Low reliability costs and focussed only on Observed and High reliability costs, to make the non-India dataset comparable with the India dataset. Since the India dataset spanned the period of 1960–2020, we further truncated the non-India dataset to the same duration. This resulted in a non-India dataset of 7450 cost records.

Subsequently, we looked at geographical, environmental, typological (damage versus management), taxonomic and linguistic differences in costs and the number of cost entries between India and the non-India dataset to assess knowledge gaps in India compared to data availability of IAS costs for the rest of the world. Geographically, data were categorised into three spatial scales: “Country” (nation-level costs), “Site” (site-specific costs) and “Diverse” (costs expressed as numerical units, spanning a few hectares to millions of hectares). Based on the invaded environment, data were categorised into “Aquatic”, “Terrestrial”, “Semi-aquatic” and “Diverse/Unspecified” (more than one of the preceding three environmental categories). Taxonomically, costs were categorised based on the Kingdom or the broad group of the IAS, resulting in seven categories: “Bacteria”, “Chromista”, “Viruses”, “Fungi”, “Plantae”, “Animalia” and “Diverse/Unspecified” (costs attributed to multiple taxa or specific taxa). Typologically, costs were categorised as “Damage”, “Management” or “Mixed” (consisting of damage and management costs). Linguistically, costs in English were contrasted with all 15 non-English language costs combined.

Results

The total economic costs incurred by IAS to the Indian economy amounted to US$ 182.6 billion (i.e., total costs) and US$ 127.3 billion (i.e., when considering Observed and High reliability costs only) (Indian Rupees ₹ 11.9 trillion and 8.3 trillion, respectively) over the period 1960–2020. The total cost (n = 300 cost entries) includes Potential costs (US$ 54.5 billion; n = 152 cost entries; 29.8% of costs) and Low reliability costs (US$ 0.8 billion; n = 52; 0.5% of costs), which were excluded from the more conservative cost estimate that includes only Observed costs and High reliability costs (n = 96; 69.7% of costs; for details on Observed and High cost entries, see sheet ‘RawDataIndia’ of Online Resource 1). In the subsequent sections, the analyses focused on this more conservative cost estimate to ensure the robustness of our conclusions.

Distribution of IAS costs

Geographical distribution

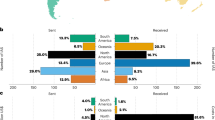

More than 99% of the economic costs were reported at the national level (US$ 126.6 billion; n = 53; 99.4%) (Fig. 1). Although most costs were estimated at the national scale, regional costs revealed that US$ 616 million were attributed to West India (n = 19; 87.5% of the regional costs), US$ 64.2 million to South India (n = 13; 9.1% of the regional costs) and US$ 23.9 million to North India (n = 11; 3.4% of the regional costs). No recorded costs were attributed to Central, Eastern, North-Eastern and Northern (claimed) India (Fig. 1). Considering all invasion-related costs of US$ 127.3 billion, the cost of invasions in India is equivalent to US$ 38,727 per km2 for the landmass of 3.287 million km2, and the per capita cost is equivalent to US$ 92.2 per inhabitant for the population of 1.38 billion Indians (2020, Worldometer). Of the five nations incurring maximum IAS costs, i.e., the USA, Australia, Brazil and China, India was second only to the USA in per unit area costs (US$ 123,048 per km2, Crystal-Ornelas et al. 2021), followed by Australia (US$ 23,790 per km2, Bradshaw et al. 2021), Brazil (US$ 9018, Adelino et al. 2021) and China (US$ 5130 per km2, Liu et al. 2021). India stood fourth in per capita costs, only ahead of China (US$ 34.9, Liu et al. 2021) and below the top three spenders, viz. Australia (US$ 7072, Bradshaw et al. 2021), the USA (US$ 3650, Crystal-Ornelas et al. 2021) and Brazil (US$ 365, Adelino et al. 2021).

Regional distribution of biological invasion costs incurred in India. Note that the costs in brackets are percentages of regional costs. Four regions have no documented cost entries (i.e., designated as NA). However, this does not infer that ‘Diverse/Unspecified’ costs were not incurred across these regions

Environmental distribution

Among the environments invaded by IAS in India, only 8% of the total entries were from diverse or unspecified environments. However, they constituted 93% of the total economic costs (i.e., Diverse/Unspecified; US$ 118 billion, n = 8). Species from semi-aquatic environments constituted only 6.7% of the total costs (US$ 8.6 billion, n = 35). Aquatic and terrestrial species-related costs were one order of magnitude lower than semi-aquatic costs, and constituted less than 1% of total costs (aquatic, US$ 509 million, n = 16; terrestrial, US$ 207 million, n = 35). One out of the 10 species in the dataset for which economic costs could be attributed occurred in semi-aquatic environments (e.g., Aedes aegypti), whereas the other nine species occurred in terrestrial environments. Economic costs could not be attributed to specific species for entries recorded under Diverse/Unspecified environments and aquatic environments.

Sectoral distribution and cost types

More than 99% of the costs affected multiple sectors and were thus classified as the “Mixed” cost type (US$ 126.8 billion, n = 48). These Mixed costs mostly comprised damage or loss related expenditures, affected diverse environments and were caused by diverse/unspecified species. Nearly all public and social welfare (US$ 344 million, n = 14) and fisheries-related costs (US$ 165.4 million, n = 2) comprised damage-related expenditures, limited to aquatic environments and caused by diverse/unspecified species. All costs incurred by the agricultural sector (US$ 39.9 million, n = 6) comprised damage-related expenditures, limited to terrestrial environments and exclusively caused by insects. The costs related to the authorities and stakeholders sector (i.e., governmental services and/or official organisations, US$ 31.1 million, n = 21) were distributed between damage and management related expenditures, mostly limited to terrestrial environments, and caused by insects. The recorded costs related to forestry were negligible in comparison to other sectors (US$ 363, n = 5). These costs were distributed between management and mixed (both damage and management) expenditures; costs were limited to terrestrial environments and solely caused by plants. The invasion costs related to the environment and health sectors were absent in uni-sectoral costs.

Taxonomic distribution

When economic costs could be attributed to a specific Kingdom, a substantial proportion (69% of cost entries) was attributed to animals (US$ 8.8 billion, n = 50; attributed to six species of insects). The majority of the animal-borne costs were attributed to Diptera (US$ 8.6 billion, n = 35; all attributed to the yellow fever mosquito, A. aegypti), Hemiptera (US$ 136 million, n = 6; attributed to the rugose spiraling whitefly, Aleurodicus rugioperculatus and the papaya mealybug, Paracoccus marginatus), Lepidoptera (US$ 38.4 million, n = 3; all attributed to the fall armyworm, Spodoptera frugiperda), Orthoptera (US$ 27.5 million, n = 5; all attributed to the desert locust, Schistocerca gregaria), and Coleoptera (US$ 3.8 million, n = 1; attributed to the coffee borer beetle, Hypothenemus hampei).

Plant costs were three orders of magnitude lower than animal costs (US$ 1.71 million, n = 22; attributed to four species of plants). The majority of costs were attributed to Poales (US$ 0.99 million, n = 6; all attributed to the littleseed canarygrass, Phalaris minor), Asterales (US$ 425, n = 11; attributed to the mile-a-minute vine, Mikania micrantha and the carrot grass, P. hysterophorus) and Lamiales (US$ 321, n = 2; attributed to lantana, Lantana camara). Three entries, amounting to US$ 0.72 million, were broadly attributed to invasive plants rather than any specific IAS. Thus, all recorded species-specific costs could be attributed to six invasive insects and four invasive plant species. No costs were explicitly recorded for fungi, bacteria, viruses and chromists. A substantial part of the costs (93%) was attributed to either unspecified taxa or taxa that covered multiple kingdoms (i.e., Diverse/Unspecified; US$ 118.5 billion; n = 24) (Fig. 2).

Cost distribution of IAS in India a showing the number of specific plant (green) and animal (purple–blue) costs recorded in InvaCost against the total number of invasive alien plants and animals present in India (grey) and b breakdown of cost by species from 1960 to 2020. Green bars represent plant costs and purple–blue bars represent animal costs. Costs are in million US$ (2017 value)

However, species-specific economic cost entries (n = 69) could only be attributed to 6 invasive animals and four invasive plants out of the 157 animal and 173 plant species that are conservatively reported to be invasive in India. This result implies that only 4% of invasive animals and 2% of invasive plants in India have species-specific documented costs based on the taxonomic resolution of the reported data. Further, the species-specific cost entries belonged to only three taxonomic classes: Insecta (72%), Magnoliopsida (19%) and Liliopsida (9% of the number of cost entries) (Fig. 2).

Species-wise cost allocations were highly skewed. Out of US$ 8.8 billion species-specific costs, the yellow fever mosquito contributed 98% of the costs, followed by the papaya mealybug at 1.5% and the fall armyworm at 0.4%. These three species also contributed maximally to management-related costs, albeit in a different order, with the papaya mealybug contributing 66% of the costs, followed by the yellow fever mosquito at 29% and the fall armyworm at 4%. More than 99% of damage costs resulted from the yellow fever mosquito, followed by the fall armyworm (0.34%) and the desert locust (0.31%) (Fig. 3).

Whittaker plot showing the proportion of IAS cost associated with a damage and b management. The proportion of cost is derived from the total cost (US$ 8.8 billion) attributed to specific species over the period 1960–2020

In terms of environments, all costs incurred from semi-aquatic taxa were caused by the yellow fever mosquito. Out of the nine species causing costs from the terrestrial environment, the highest costs were attributed to insects, with the papaya mealybug contributing 66% of the costs, followed by the fall armyworm (18%) and the desert locust (13%). All incurred costs from aquatic taxa were attributed to Diverse/Unspecified, and as such, the species-wise cost apportionment for aquatic environments was not possible (Fig. 3).

Introduction pathways

Nine of the ten IAS were introduced to India via humans, while the only IAS that naturally expanded its range in South Asia and India was S. gregaria due to the changing climate (Meynard et al. 2020). Seven IAS were introduced unintentionally as a result of unaided transport via trade or tourism, of which six arrived as contaminants of seeds and live material (i.e., A. rugioperculatus, H. hampei, P. marginatus, P. hysterophorus, P. minor, and S. frugiperda), whereas A. aegypti arrived via stowaway. The remaining two species were intentionally released in India during British rule (L. camara, M. micrantha) (Table 1).

Temporal trends

On average, damage expenditures amounted to US$ 2.1 billion annually from 1960 to 2020, increasing from US$ 0.6 million per year in the 1960s and escalating to US$ 12.3 billion in the 2000s (Fig. 4). While management costs also increased, their reporting began three decades later than damage costs, averaging at US$ 4.1 million overall to US$ 13.2 million in the 2010s. Management costs were always at least one order of magnitude below damages (Fig. 4). Considering models of the temporal trends in total costs, the amplitude of reported costs increased as the quantiles became more divergent. Thus, costs became more variable, making 2020 estimations of costs differ substantially among models (see Online Resource 2). Excepting multivariate adaptive regression splines, which declined in recent years potentially due to sensitivity to time lags, all models displayed an increase in costs over time.

Temporal trends depicting damage and management costs of invasive alien species in India. Bars represent 10-year averages; points represent annual totals, with size scaled by numbers of cost entries per year; the dashed lines represent the trends between bars. No data was available for the decade of 1970–1980. Note that the y-axis is on a log10 scale

Cost extrapolation for IAS with no recorded costs in India

The cost relationship between India and the rest of the world was:

By extrapolating the global costs to 54 IAS (out of the 330 IAS from India) having no recorded costs in India with the above equation, our estimations predict that these 54 IAS have caused an additional minimum potential economic burden of US$ 952 million in the last 60 years.

Association with socioeconomic status

There was a significant positive relationship between economic cost and total human population across countries in InvaCost [F(1, 107) = 57.416, p < 0.001], independent of economic development status as a two-way interaction [F(2, 107) = 1.433, p = 0.243]. Economic costs of IAS were also significantly positively related with GDP [F(1, 107) = 58.597, p < 0.001], but not when the economic development was included as an interaction [F(2, 107) = 0.660, p = 0.519]. Accordingly, the strength of these population-cost and GDP-cost relationships were independent of economic development status (i.e., developed, developing, transitioning).

Nonetheless, India had the second-highest national total costs caused by IAS considering all countries in InvaCost (Fig. 5), only second to the USA, with costs generally low in relation to both human population density and GDP. Indeed, given the strong correlation between economic costs and total human population and GDP, costs of IAS in India are projected to have reached between US$ 3.4 trillion (based on GDP) and US$ 1700 trillion (based on human population), predicated on the relationship considering all countries. The top five countries in InvaCost in terms of total economic costs include the USA, India, Australia, Brazil and China. Compared to India, total invasion costs among these countries are generally underrepresented in terms of the total human population (except for Australia) and GDP (Fig. 5).

National economic total costs caused by IAS from 1960 to 2020 in relation to a total human population and b GDP. Note that both y-axes are on logn scales. India, the USA, China, Brazil and Australia are highlighted for comparison. Dashed lines correspond to linear regressions, irrespective of economic development status. Economic costs caused by IAS in all the countries considered here were extracted from the InvaCost database

Knowledge gaps

Geographically, 96% of non-India costs and > 99% of India’s costs were reported at the national level (Fig. 6). However, when analysed for the number of cost entries, the differences between the two datasets were more evident. Only 18% of non-Indian cost entries were reported at the national level to 47% of national level costs in the Indian dataset. Inversely, 72% of non-India cost entries were reported at site-level, whereas it was only 21% of site-level cost entries for India. Environmentally, the “Diverse/Unspecified” category accounts for 92% of India’s costs, but just 2% of non-India costs (Fig. 6). 98% of the non-India costs are assigned to specific invaded environments. The main difference between the non-India and the India costs was that costs in aquatic and terrestrial environments in the non-India dataset constituted a substantial percentage of total costs (44% and 46% of total costs, respectively). In contrast, together, these two environments constituted less than 1% of total costs in India.

Comparison of distribution of costs according to geographic scale, language of cost reporting, type of cost, invaded environment, and taxon, within India and outside India

Similarly, the “Diverse/Unspecified” taxonomic category, where costs were not assigned at all or were not assigned to a single Kingdom, constituted 93% of India’s total IAS costs but constituted only 50% of the non-India costs (Fig. 6). Typologically, damage-related costs were high in both datasets. However, the main difference between the two datasets was in the representation of management and mixed costs. Management and mixed costs constituted less than 0.2% for India but accounted for more than 20% of the non-India costs (Fig. 6).

Similar to geographic differences between India and non-India costs, differences in costs based on the language of reporting remained hidden when only the amount of the cost was analysed, but these differences became more apparent when the number of cost entries was analysed. Costs reported in English dominated non-India and India data (97% and 99.9% of total costs, respectively) (Fig. 6). However, more than 67% of the total number of the non-India cost entries were reported in non-English languages, whereas only 2% of the India cost entries were in non-English languages.

In summary, in addition to the important gaps in costs, a very high proportion of the recorded costs in India were provided with insufficient details to allow analyses of different variables, such as taxonomy of the invasive species, locality of the invasion or activity sector impacted.

Discussion

Massive yet underestimated costs

IAS cost the Indian economy at least US$ 127.3 billion (Indian Rupees ₹ 8.3 trillion) from 1960 to 2020, with an average annual amount of US$ 2.1 billion. If low reliability and potential costs were included in the aforementioned conservative cost estimates, the costs escalate to US$ 182.6 billion (Indian Rupees ₹ 11.9 trillion), thus costing more than US$ 3 billion annually over the last six decades. These costs are an enormous burden not just on the Indian economy, but also on global economic growth and development. For example, the average annual IAS cost estimate of US$ 2.1 billion in India is higher than the national GDPs of 25 of the world’s smallest economies (International Monetary Fund 2021). In a global ranking of countries incurring IAS costs, India occupies the second rank, and incurs more costs as a result of IAS than the whole of continental Europe (US$ 125.6 billion) (Haubrock et al. 2021a) or Africa (US$ 18.8 billion) (Diagne et al. 2021b). Nonetheless, we should keep in mind that relevant geographic comparisons of costs should take into account differences in values of money between areas as well as local specificities, such as invasion histories or economic and research capacities dedicated to IAS (Diagne et al. 2021b).

When expressed as a percentage of the national GDP of India, the IAS costs may appear deceptively small at 0.08% of the national GDP of India (i.e., US$ 2.9 trillion; International Monetary Fund 2020); however, the severity of these costs is clearer when compared with the operational measures undertaken by India for environmental conservation. For example, the annual estimated costs of US$ 2.1 billion was an order of magnitude higher than the 2021–2022 yearly allocated budget of the Government of India’s Ministry of Environment, Forestry and Climate Change (i.e., Indian Rupees ₹ 28.7 billion or US$ 0.4 billion) (Government of India 2021). Additionally, there is a possibility of disregarding the severity of IAS costs by comparing them with costs incurred by other environmental disasters. For example, annual climate change-related costs in India are estimated at US$ 99 billion (Chaturvedi 2015). However, in India, costs of climate change impacts have been assessed extensively, while costs of biological invasions are grossly under-investigated.

Indeed, our results suggest that these estimates are likely a small fraction of actual invasion-related costs in the country. Firstly, as far as we are aware, this study is the first attempt at calculating invasion costs that are observed and highly reliable. It follows that more efforts to collect and curate similar data will lead to higher costs. Secondly, the methods were stringent and included several levels of filtering to achieve the most reliable costs for this study. Of the 300 cost entries derived from 73 unique cost-based references, we excluded 204 cost entries from 51 references from the final analysis to keep only the most complete and reliable data. This means that the cost amounts shown here are highly conservative, given we focused on a portion of the original dataset. Thirdly, the data were geographically, taxonomically and sectorally fragmented, leading to likely underestimated costs (see details in the following sections). Fourthly, language barriers can cause gaps in information availability, and this is likely the case for India—only 2 of the 73 unique references included non-English languages (both in Hindi). However, only one non-English reference was included in the final analysis due to reliability issues. In a linguistically-diverse country such as India, with 22 official regional languages, many cost entries, especially the regional and local costs, are possibly documented in regional languages and overlooked. Additionally, searching for costs was difficult because appropriate parallel regional language terms for ‘invasive species’ or ‘biological invasions’ do not exist. Accordingly, it has been shown that up to twice as many cost entries could be found in non-English sources in the InvaCost database (Angulo et al. 2021). Lastly, InvaCost only considers those cost entries which were directly attributable to IAS and could be monetised. IAS may impact native ecosystems in ways that are difficult to monetise, such as declines in ecosystem services or native species populations. Alternatively, they may cause quantifiable but indirect impacts, where attribution of species costs or invasion status may be secondary. The above-mentioned reasons suggest that the current cost projections reflect only a fraction of the actual costs and are thus grossly underestimated. An illustration of this is revealed by the global analysis of invasion costs relative to socioeconomic indicators such as total human population and GDP. The costs of IAS in India are severely underestimated, by at least an order of magnitude—compared to what would be expected considering all other countries with invasion costs.

Widespread knowledge gaps in the distribution of costs

Most cost entries lacked information accompanying costs, such as exact location and spatial scale, impacted environments, identification of the causal organism to species level, type of cost, and impacted sector. In most cases, the costs were attributed to the “diverse/unspecified” category, meaning that either the costs were calculated over multiple categories without the break-up amount per category, or more challengingly, these attributes were not specified. This lack of information is a problem as it is difficult to design action plans specific to regions, ecosystems, species, and sectors. While these results add to our knowledge, these results need to be approached with caution. The fragmentary nature of economic cost distributions suggests that the availability of more invasion-cost related information may change the trends and knowledge gaps observed in this study.

More broadly, existing global biases in the documentation of economic impacts for particular regions, taxa, environments and sectors are inevitably reflected in the InvaCost database—given its dependency on published records—and, therefore, these also exist in the India dataset. For instance, costs in anthropocentric sectors such as agriculture, public and social welfare, and authorities-stakeholders outweigh costs in sectors such as the environmental sector. Another example of the underrepresentation of costs is seen in research and education-related funding, which is mostly unavailable in the literature, and hence, underrepresented in InvaCost and the India dataset. Such knowledge gaps are problematic but will decline as more efforts are taken to document, compile and synthesise IAS costs.

Geographical distribution

About 99.5% of costs and nearly half of the total number of cost entries in India have been reported at the country level and not at the regional or provincial levels. National level costs, as opposed to site-specific costs pertaining to smaller areas, have caused the greatest costs globally, also observed in non-India costs. This is expected as national level costs will be higher than site-level costs owing to larger areas. However, the problematic part for India is the number of cost entries at the national level versus for specific sites, and in this regard, India and non-India costs are markedly different. The number of site-specific costs in India are about a quarter (18%) of the numbers of site-specific costs found outside India (72%), indicating a much finer resolution in the assignment of costs to specific sites outside India. Although the India dataset used in this study is relatively small, it is indicative of a broad stroke in assigning costs to the entire country rather than to specific sites, thereby making it challenging to design an effective IAS management plan.

Although the regional or local costs were only a fraction of the national level costs, there were marked differences among the six administrative regions of India. All regional or local cost entries were reported from West, South and North Indian regions, without any costs associated with Central, East or North-East India. This biased geographic distribution of costs could result from the preliminary nature of this study and a small dataset, but there could be other reasons involved. Coincidentally, these three regions with attributable costs contribute to about 80% of India’s GDP (2018–2019 estimates; South India 29.9%, North India 27.2% and West India 22.2% of India’s total Gross State Domestic Product). These three regions also share most of the inland and international trade (e.g., West India contributes 40%, and South India contributes about 30% of India’s export of goods and services). Consequently, these regions may contain more IAS, and as a result, more cost entries are reported from these regions. Moreover, even if IAS are uniformly distributed across India, the availability of monetary resources to offset and record invasion costs may suffice to make these three regions more represented in the dataset.

Environmental distribution

Although terrestrial invaders are maximally represented in our data (n = 37), followed by those from semi-aquatic (n = 35) and aquatic environments (n = 16), the costs borne from taxa inhabiting terrestrial environments were half of those borne by aquatic taxa and over 40-fold less than semi-aquatic environments. This break-up of costs indicates that invasions by semi-aquatic and aquatic taxa have been causing a greater monetary burden to the economy, yet they are primarily understudied. However, importantly, the semi-aquatic costs were driven solely by a single species, the yellow fever mosquito, reflecting the substantial human healthcare costs associated with this taxon—which has aquatic juvenile stages—and corroborating previous studies (Bradshaw et al. 2016; Cuthbert et al. 2021b). Nevertheless, the underrepresentation of aquatic and semi-aquatic ecosystems in studies on biological invasions is not unique to India, as these ecosystems are less represented in ecological literature than terrestrial ecosystems (Menge et al. 2009). More specifically, in the context of IAS, aquatic ecosystems, and in particular marine ones, might be underrepresented as well because these invasions might be less perceptible or costs are challenging to measure, thus, more likely to be predicted than observed (Oreska and Aldridge 2011; Cuthbert et al. 2021b).

We found distinct differences in the cost apportionment in invaded environments between India and non-India costs. Globally, less than 2% of costs are assigned to “Diverse/Unspecified” environments, whereas, in India, ~ 93% of costs are assigned to this category, making it challenging to address invasion-borne costs. The proportion of costs in semi-aquatic environments is comparable between India and non-India costs. Possibly, costs categorised as “Diverse/Unspecified” environments in India could have all come from terrestrial and aquatic environments, which together form ~ 90% of non-India costs but less than 1% of India costs. Although the India dataset is preliminary and small, such poor representation of terrestrial and aquatic costs and a very high percentage of unassigned environmental costs is a two-fold impediment in restoring invaded environments.

Sectoral distribution and cost types

More than 99% of costs affected multiple sectors and were therefore classified as “mixed costs”. For example, costs resulting from the yellow fever mosquito are borne by the health sector; however, they also burden authorities and stakeholders. Even if the cost is reported to have impacted only one sector, delayed effects might impact other sectors. For example, Eichhornia and many other exotic weeds have affected the fisheries sector but have also caused a steady decline in the tourism sector that relies on aquatic ecosystems. Thus, these mixed costs point to the multi-pronged nature of the impacts of biological invasions, possibly leading to a socioeconomic domino effect, especially in an emerging economy. Among uni-sectoral costs, maximum costs were attributed to anthropocentric sectors such as public and social welfare, fisheries, agriculture, and authorities and stakeholders. Sectors such as forestry and environment were either negligible in terms of amount and number of costs or completely absent from the records. This bias indicates selective reporting from anthropocentric sectors and difficulty in monetising costs in non-anthropocentric sectors such as forestry and the environment. As the dataset on the economic costs associated with IAS in India grows, these trends may change. It is pertinent to note that the cost assessment in this study is more realistic and evidence-based than many earlier attempts that attributed colossal costs to IAS in India, since such studies relied on extrapolations of existing costs, or on the estimation of potential (i.e., not actually realised) costs. For example, Pimentel et al. (2001) proposed that the agricultural sector in India experiences annual costs of US$ 90 billion. While this estimation could be potentially valid, the main criticism levelled against it and many other cost estimation studies globally has been that they report potential costs and not realised observed costs. Since the actual documentary evidence for the monetary impacts due to invasions is missing, the criticism then is that these figures from earlier studies could be a gross overestimation of real costs. In comparison, our study reports that the observed and highly reliable annual agricultural costs reported in India caused by IAS amount to US$ 6.5 million. Even if we accounted for costs that are classified as multi-sectoral (“diverse/unspecified”) and where agriculture is one of the several affected sectors, and used them within the ambit of agricultural costs, the annual agricultural cost would amount to US$ 1.97 billion—still only a fraction of the agricultural cost suggested by Pimentel et al. (2001). It is important to note that potential costs projected by earlier studies, and estimation of documented costs by our study are not incompatible, but they highlight two different aspects of the problem posed by IAS, viz., the potential economic impact and the observed economic impact. Such evidence-based observed cost assessments as performed in our study, as opposed to extrapolative cost assessments done in earlier studies, are likely to be more agreeable to formulating realistic policies around this issue.

Globally, damage costs caused by IAS dominate the cost data as compared to management-related costs of these species and India follows this pattern. The extent of this skew in India is, however, worrying. Globally, ~ 22% of total costs are incurred by management-related expenses, whereas in India it forms less than 0.2% of total costs. However, a further dip in the apportionment of management-related costs in India as compared to the global percentages is indicative of another problematic area regarding spending on research, education, surveillance, and eradication efforts. As the India cost database grows, it will be discernible if this trend is real or has arisen due to a lack of enough data.

Taxonomic distribution

More than 95% of India’s invasive animals and plants did not have a single documented cost. Similar patterns have been observed in invasion-related costs in the UK (Cuthbert et al. 2021a), Australia (Bradshaw et al. 2021), Russia (Kirichenko et al. 2021), France (Renault et al. 2021), Mexico (Rico-Sánchez et al. 2021) or Argentina (Duboscq-Carra et al. 2021). Out of the 157 invasive animal species in India, 99 are reported from marine environments. Although the database has cost entries from marine environments, the species responsible for these costs were categorised as diverse or unspecified. Indeed, considering the entire database globally, marine species comprise only approximately 1% of total aquatic invasion costs (Cuthbert et al. 2021b), indicating a paucity in reporting their costs, or fewer human assets that are impacted in the marine realm. Further actions to tackle these costs become challenging because the IAS to be controlled are unknown. The 58 invasive animals found in India in terrestrial and freshwater ecosystems include 31 arthropod species, three molluscs, 19 fish species, 1 reptile, 2 birds and 2 mammalian species (Government of India 2018). Except for arthropods (all belonging to class Insecta), none of the other taxa had any representation in InvaCost.

The total absence of mammals from this estimate, when they are the second most costly order globally (Diagne et al. 2021a), is striking in this regard. The representation was worse for Fungi and Chromista, and viruses, since no cost entry was attributed to these entire Kingdoms. Only three of the 21 HiCIS from India (Mungi et al. 2019) had cost entries in our dataset. If low reliability and potential costs were considered, three more species from HiCIS would be included, viz., Achatina fulica, Eichhornia crassipes and Prosopis juliflora. Despite probably high actual costs, the remaining 15 HiCIS did not have a single cost entry in our dataset. Even focused species-wise searches on the economic impacts of the remaining HiCIS did not reveal costs.

Globally, ~ 50% of costs can be assigned to specific taxa, however, in India, only ~ 7% of species have taxon-specific costs. The knowledge gap regarding the costs of invasive plants in India is another problematic area. Although costs incurred by plants form ~ 23% of the cost entries for India, they constitute only 0.001% of total costs. This is also worrisome when compared with the 15% share of invasive plant costs from the rest of the world. This is indicative of the undervaluation of invasive plant costs and this knowledge gap in India needs further attention.

Introduction pathways

One of the considered species, S. gregaria, has increased its range in India due to climatic changes. We have nonetheless included it in this estimation because species expanding due to climate change are sometimes considered IAS since climate change is human-made (Hulme 2015; but also see Essl et al. 2019); yet, its exclusion would have changed neither our overall results nor our conclusions.

With increased foreign investment and decreased import tariffs, India’s share in international trade has increased substantially. India is currently ranked 8th in the world in international trade imports. The impetus for international trade has not developed alongside international and national policy guidelines related to biological invasions. For example, policies of different international agencies may conflict with each other, such as those of the World Trade Organization (WTO) promoting an unrestricted movement of products and those of the Convention on Biological Diversity (CBD) and the Convention on International Trade in Endangered Species of Wild Fauna and Flora (CITES) promoting regulation of these movements (Hulme 2007; Hulme et al. 2018). Many of these policies also consider economic impacts in managed ecosystems such as agriculture, livestock and fisheries, but not economic impacts and biodiversity losses in natural ecosystems such as forests. Consequently, species that only affect natural ecosystems often do not come under the direct purview of many of these policies and may not be blacklisted (Hulme 2007).

Along with international trade, India also serves as a global hub for tourism, with an annual turnover of 17 million inbound foreign tourists and 26 million outbound Indian tourists (Government of India 2019). The inbound contaminants via trade and tourists are usually targeted via the international sanitary standards as a part of the border quarantine protocols. However, developing potential IAS lists and a ‘whitelist’ approach, wherein every contaminant or contaminate species is considered potentially dangerous unless proved safe via risk profiling, will be more effective than relying on ‘blacklisted’ species. Adopting a ‘whitelisting’ approach is more stringent and hence more effective in controlling potential invasions (Simberloff 2006; Hulme et al. 2018), and hence, is proposed to be implemented in trade-related movements of species (Bang and Courchamp 2021).

Temporal trends

Overall, reported costs have increased by five orders of magnitude over the last six decades in India. The increase in the invasion costs over time could be a result of an increasing number of IAS entering, establishing and spreading in India, increased numbers of reports and studies on IAS and their costs, as well as inadequate legal and policy frameworks to prevent them.

The break-up of costs revealed that the rate of increase in the damage-loss type of costs has been substantially higher than the management-related costs. Moreover, management costs have always been one-four orders of magnitude less than damage-loss costs, and this is quite telling of the problem related to IAS in India. It is well established that spending on pre-entry measures is more cost-effective than on longer-term post-entry responses (Leung et al. 2002; Ahmed et al. 2022), and thus preventative measures should be given priority. As newer species accumulate, existing species spread and “invasion debts” increase due to a delayed impact of IAS (Seebens et al. 2017), and increased world trade and climate change exacerbate biological invasions, their costs are also likely to further increase with time.

Association with socioeconomic status

A key finding emerging from our results is the significant positive association between invasion costs incurred by a country and its total population and GDP. Anthropogenic impacts affect biological invasions, with more populous and dense regions comprising higher numbers of IAS (Pyšek et al. 2010; Sharma et al. 2010). Furthermore, a high GDP and high volumes of international trade result in higher international imports and thus provide more opportunities for introducing IAS (Haubrock et al. 2021b, 2021c; Kouranditou et al. 2021). India is currently ranked 8th in international imports and currently ranks in the top four countries on many national transport-related measures such as total road network, total rail network, total passengers carried via air transport annually, among other measures (https://data.worldbank.org/indicator/IS.AIR.PSGR). This inland transport network implies that once a non-native species gains entry, it may quickly spread to the distant corners of the country, leading to higher overall invasion costs.

Despite India being the second topmost country globally regarding invasion costs, the invasion costs are less based on its total population and GDP relative to other countries. Indeed, relative to the global trend, costs in India from invasions are substantially underreported—by several orders of magnitude—with respect to GDP and human population. Considering the international regressions between costs, population and GDP using InvaCost and socio-economic data for other countries in the database, observed costs in India could have, in fact, reached costs several magnitudes higher. Costs were particularly unrepresented considering the substantial total human population of India, which is a significant predictor of the economic costs of IAS on the global scale. Other countries that reported the highest invasion costs, namely the USA, Brazil and China, also had underestimated costs relative to the human population, and it was also the case for Australia relative to its GDP. India was most similar to China in terms of underreporting cost magnitudes relative to the total human population—both having high population levels—but clustered with Australia and Brazil, given similarities in GDP. Overall, this indicates that even for countries with a high total economic output and human population, costs of IAS tend to be severely underestimated, which is exemplified considering India.

Conclusion

Comparable to many other developing economies, India faces the conundrum of the simultaneous pursuit of economic development and environmental conservation. Although ecological impacts of biological invasions are increasingly recognised, the economic burdens they create are often challenging to comprehend, assess, quantify, and integrate into the national policy. The knowledge gaps in the reporting on economic costs are pervasive in India, as seen by the lack of geographical, environmental, sectoral, taxonomic and linguistic specificity of costs. These gaps need to be addressed swiftly, primarily due to the escalating nature of IAS costs with time. India is the second topmost country regarding IAS costs, and even these costs are likely to be a gross underrepresentation of the actual costs based on our global analysis of 112 countries. In addition to the dire environmental impact of IAS, they are also a critical hindrance to the economic development of this emerging economy. Prioritising IAS management will slow the rate of new incursions and reduce the impacts of IAS instead of prioritising damage costs which will continue to escalate over time. To this end, it is crucial to build better national policies related to international trade, improve the existing border biosecurity and sanitary protocols, develop early-response programmes to contain IAS that have already gained entry, foster agencies and human resources devoted to creating and disseminating knowledge on IAS, and finally, strengthen research and knowledge generation by launching a nationwide programme around invasion science in India.

Data availability

The data used for analyses are provided in the Supplementary Material (ESM_1). The scripts used for analyses are included in the ‘invacost’ package in R (https://doi.org/10.1101/2020.12.10.419432). Any further information can be obtained from the request to the authors.

References

Adelino JRP, Heringer G, Diagne C, Courchamp F, Faria LDB, Zenni RD (2021) The economic costs of biological invasions in Brazil: a first assessment. In: Zenni RD, McDermott S, García-Berthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:349–374

Ahmad R, Khuroo AA, Hamid M, Charles B, Rashid I (2019) Predicting invasion potential and niche dynamics of Parthenium hysterophorus (Congress grass) in India under projected climate change. Biodivers Conserv 28(8):2319–2344

Ahmed DA, Hudgins EJ, Cuthbert RN, Kourantidou M, Diagne C, Haubrock PJ, Leung B, Liu C, Leroy B, Petrovskii S, Beidas A, Courchamp F (2022) Managing biological invasions: the cost of inaction. Biol Invasions. https://doi.org/10.1007/s10530-022-02755-0

Angulo E, Diagne C, Ballesteros-Mejia L, Adamjy T, Ahmed DA et al (2021) Non-English languages enrich scientific knowledge: the example of economic costs of biological invasions. Sci Total Environ 775:144441

Bang A, Courchamp F (2021) Industrial rearing of edible insects could be a major source of new biological invasions. Ecol Lett 24:393–397

Bellard C, Cassey P, Blackburn TM (2016) Alien species as a driver of recent extinctions. Biol Lett 12(2):20150623

Booth BD, Murphy SD, Swanton CJ (2003) Plant invasions. In: Booth BD, Murphy SD, Swanton CJ (eds) Weed ecology in natural and agricultural systems. CABI, Oxford, pp 235–253

Botanical Survey of India (n.d.) Invasive alien species. Botanical Survey of India. http://www.bsienvis.nic.in/Database/Invasive_Alien_species_15896.aspx. Accessed 21 March 2021

Bradshaw CJ, Leroy B, Bellard C, Roiz D, Albert C et al (2016) Massive yet grossly underestimated global costs of invasive insects. Nat Commun 7(1):1–8

Bradshaw CJA, Hoskins AJ, Haubrock PJ, Cuthbert RN, Diagne C, Leroy B, Andrews L, Page B, Cassey P, Sheppard AW, Courchamp F (2021) Detailed assessment of the reported economic costs of invasive species in Australia. In: Zenni RD, McDermott S, García-Berthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:511–550

Brooks ML, D’Antonio CM, Richardson DM, Grace JB, Keeley JE, DiTomaso JM, Hobbs RJ, Pellant M, Pyke D (2004) Effects of invasive alien plants on fire regimes. Bioscience 54:677–688

Capinha C, Essl F, Seebens H, Moser D, Pereira HM (2015) The dispersal of alien species redefines biogeography in the Anthropocene. Science 348:1248–1251

Chaturvedi V (2015) The costs of climate change impacts for India. https://www.ceew.in/sites/default/files/CEEW-The_Costs_of_Climate_Change.pdf

Choudhury AK (1972) Controversial Mikania (climber)—a threat to the forests and agriculture. Indian for 98(3):178–186

Crystal-Ornelas R, Lockwood JL (2020a) The ‘known unknowns’ of invasive species impact measurement. Biol Invasions 22(4):1513–1525

Crystal-Ornelas R, Lockwood JL (2020b) Cumulative meta-analysis identifies declining but negative impacts of invasive species on richness after 20 years. Ecology 101(8):e03082

Crystal-Ornelas R, Hudgins EJ, Cuthbert RN, Haubrock PJ, Fantle-Lepczyk J, Angulo E, Am K, Ballesteros-Mejia L, Leroy B, Leung B, López-López E, Diagne C, Courchamp F (2021) Economic costs of biological invasions within North America. In: Zenni RD, McDermott S, García-Berthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:485–510

Cuthbert RN, Bartlett AC, Turbelin AJ, Haubrock PJ, Diagne C, Pattison Z, Courchamp F, Catford JA (2021a) Economic costs of biological invasions in the United Kingdom. In: Zenni RD, McDermott S, García-Berthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:299–328

Cuthbert RN, Pattison Z, Taylor NG, Verbrugge L, Diagne C et al (2021b) Global economic costs of aquatic invasive alien species. Sci Total Environ 775:e145238

Diagne C, Catford JA, Essl F, Nuñez MA, Courchamp F (2020a) What are the economic costs of biological invasions? A complex topic requiring international and interdisciplinary expertise. NeoBiota 63:25

Diagne C, Leroy B, Gozlan RE, Vaissière AC, Assailly C et al (2020b) InvaCost, a public database of the economic costs of biological invasions worldwide. Sci Data 7(1):1–12

Diagne C, Leroy B, Gozlan RE, Vaissière AC, Assailly C et al (2020c) InvaCost: references and description of economic cost estimates associated with biological invasions worldwide. Figshare Dataset. https://doi.org/10.6084/m9.figshare.12668570.v3

Diagne C, Leroy B, Vaissière AC, Gozlan RE, Roiz D, Jarić I, Salles JM, Bradshaw CJA, Courchamp F (2021a) High and rising economic costs of biological invasions worldwide. Nature 592(7855):571–576

Diagne C, Turbelin AJ, Moodley D, Novoa A, Leroy B, Angulo E, Adamjy T, Dia CAKM, Taheri A, Tambo J, Dobigny G, Courchamp F (2021b) The economic costs of biological invasions in Africa: a growing but neglected threat? In: Zenni RD, McDermott S, GarcíaBerthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:11–51

Duboscq-Carra VG, Fernandez RD, Haubrock PJ, Dimarco RD, Angulo E, Ballesteros Mejia L, Diagne C, Courchamp F, Nuñez MA (2021) Economic impact of invasive alien species in Argentina: a first national synthesis. In: Zenni RD, McDermott S, García-Berthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:329–348

Early R, González-Moreno P, Murphy ST, Day R (2018) Forecasting the global extent of invasion of the cereal pest Spodoptera frugiperda, the fall armyworm. NeoBiota 40:25–50

Essl F, Dullinger S, Genovesi P, Hulme PE, Jeschke JM, Katsanevakis S, Kühn I, Lenzner B, Pauchard A, Pyšek P, Rabitsch W (2019) A conceptual framework for range-expanding species that track human-induced environmental change. Bioscience 69(11):908–919

Fantle-Lepczyk JE, Haubrock PJ, Kramer AM, Cuthbert RN, Turbelin AJ, Crystal-Ornelas R, Diagne C, Courchamp F (2022) Economic costs of biological invasions in the United States. Sci Total Environ 806(2022):151318

Finch EA, Beale T, Chellappan M, Goergen G, Gadratagi BG, Khan MA, Rehman A, Rwomushana I, Sarma AK, Wyckhuys KA, Kriticos DJ (2021) The potential global distribution of the papaya mealybug, Paracoccus marginatus, a polyphagous pest. Pest Manag Sci 77(3):1361–1370

Ganie MA, Bhat MD, Khan MI, Parveen M, Balkhi MH, Malla MA (2013) Invasion of the Mozambique tilapia, Oreochromis mossambicus (Pisces: Cichlidae; Peters, 1852) in the Yamuna River, Uttar Pradesh, India. J Ecol Nat 5(10):310–317

Government of India, Department of Agriculture, Cooperation and Farmers’ Welfare (2013) Locust warning organization. https://agricoop.gov.in/sites/default/files/Locust%20Warning%20Organization_0.doc. Accessed 21 March 2021

Government of India (2018) Invasive animal species. http://164.100.24.220/loksabhaquestions/annex/13/AU3124.pdf. Accessed 21 March 2021

Government of India, Ministry of Tourism (2019) India tourism statistics. https://tourism.gov.in/sites/default/files/2020-04/India%20Tourism%20Statistics%202019.pdf. Accessed 21 March 2021

Government of India, Ministry of Finance (2021). https://www.indiabudget.gov.in/doc/eb/sbe27.pdf. Accessed 21 March 2021

Goyal N, Krishna S, Shah K, Rashid I, Sharma GP (2021) Integrating the biological invasion paradigm in the policy framework in India. Trop Ecol 62(1):144–148

Haubrock PJ, Turbelin AJ, Cuthbert RN, Novoa A, Taylor NG, Angulo E, Ballesteros Mejia L, Bodey TW, Capinha C, Diagne C, Essl F, Golivets M, Kirichenko N, Kourantidou N, Leroy B, Renault D, Verbrugge L, Courchamp F (2021a) Economic costs of invasive alien species across Europe. In: Zenni RD, McDermott S, GarcíaBerthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:153–190

Haubrock PJ, Cuthbert RN, Sundermann A, Diagne C, Golivets M, Courchamp F (2021b) Economic costs of invasive species in Germany. In: Zenni RD, McDermott S, GarcíaBerthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:225–246

Haubrock PJ, Cuthbert RN, Yeo DCJ, Banerjee AK, Liu C, Diagne C, Courchamp F (2021c) c) Biological invasions in Singapore and Southeast Asia: data gaps fail to mask potentially massive economic costs. In: Zenni RD, McDermott S, García-Berthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:131–152

Heringer G, Angulo E, Ballesteros-Mejia L, Capinha C, Courchamp F, Diagne C, Duboscq-Carra VG, Nuñez MA, Zenni RD (2021) The economic costs of biological invasions in Central and South America: a first regional assessment. In: Zenni RD, McDermott S, García-Berthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:401–426

Hoagland P, Jin D (2006) Science and economics in the management of an invasive species. Bioscience 56(11):931–935

Hoffmann BD, Broadhurst LM (2016) The economic cost of managing invasive species in Australia. NeoBiota 31:1

Holmes TP, Aukema JE, Von Holle B, Liebhold A, Sills E (2009) Economic impacts of invasive species in forest past, present, and future. In: The year in ecology and conservation biology, 2009. Ann NY Acad Sci 1162:18–38

Hulme PE (2007) Biological invasions in Europe: drivers, pressures, states, impacts and responses. In: Hester R, Harrison R (eds) Biodiversity under threat. Cambridge University Press, Cambridge, pp 56–80

Hulme PE (2015) Invasion pathways at a crossroad: policy and research challenges for managing alien species introductions. J Appl Ecol 52(6):1418–1424

Hulme PE, Brundu G, Carboni M, Dehnen-Schmutz K, Dullinger S et al (2018) Integrating invasive species policies across ornamental horticulture supply chains to prevent plant invasions. J Appl Ecol 55:92–98

International Monetary Fund (2020) World Economic Outlook Database. https://www.imf.org/en/Publications/WEO/weo-database/2020/October/weo-report?c=534,&s=NGDP_RPCH,NGDPD,PPPGDP,NGDPDPC,PPPPC,PCPIPCH,&sy=2021&ey=2021&sort=country&ds=.&br=1. Accessed 21 March 2021

International Monetary Fund (2021) World Economic Outlook Database. https://www.imf.org/external/datamapper/NGDPD@WEO/OEMDC/ADVEC/WEOWORLD. Accessed 2 Oct 2021

Johnson MA, Ruiz-Diaz CP, Manoukis NC, Verle Rodrigues JC (2020) Coffee berry borer (Hypothenemus hampei), a global pest of coffee: perspectives from historical and recent invasions, and future priorities. Insects 11(12):882

Kaushik S, Blackshaw RE, Inderjit, (2005) Ecology and management of an exotic weed Phalaris minor. In: Inderjit S (ed) Invasive plants: ecological and agricultural aspects. Birkhäuser, Basel, pp 181–193

Kirichenko N, Haubrock PJ, Cuthbert RN, Akulov E, Karimova E, Shneider Y, Liu C, Angulo E, Diagne C, Courchamp F (2021) Economic costs of biological invasions in terrestrial ecosystems in Russia. In: Zenni RD, McDermott S, García-Berthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:103–130

Kohli RK, Batish DR, Singh HP, Dogra KS (2006) Status, invasiveness and environmental threats of three tropical American invasive weeds (Parthenium hysterophorus L., Ageratum conyzoides L., Lantana camara L.) in India. Biol Invasions 8(7):1501–1510

Kourantidou M, Cuthbert RN, Haubrock PJ, Novoa A, Taylor NG, Leroy B, Capinha C, Renault D, Angulo E, Diagne C, Courchamp F (2021) Economic costs of invasive alien species in the Mediterranean Basin. In: Zenni RD, McDermott S, García-Berthou E, Essl F (eds) The economic costs of biological invasions around the world. NeoBiota 67:427–458

Kumar PK, Prakasan CB, Vijayalakshmi CK (1990) Coffee berry borer Hypothenemus hampei (Coleoptera: Scolytidae): first record from India. J Coffee Res 20(2):161–164

Kumschick S, Gaertner M, Vilà M, Essl F, Jeschke JM et al (2015) Ecological impacts of alien species: quantification, scope, caveats, and recommendations. Bioscience 65(1):55–63

Leroy B, Kramer AM, Vaissière AC, Courchamp F, Diagne C (2020) Analysing global economic costs of invasive alien species with the invacost R package. bioRxiv

Leung B, Lodge DM, Finnoff D, Shogren JF, Lewis MA, Lamberti G (2002) An ounce of prevention or a pound of cure: bioeconomic risk analysis of invasive species. Proc R Soc Lond B 269(1508):2407–2413